The global economy stands at a critical juncture, where technical market patterns, runaway inflation, and technological shifts are converging to reshape the financial landscape. This article explores a potential, but from our analysis a likely scenario of how it might unfold, including the current state of the markets, the looming threat of hyperinflation, the potential collapse of traditional financial systems, the rise of Central Bank Digital Currencies (CBDCs) as a surveillance-heavy solution, and the role cryptocurrencies—particularly privacy coins like Ryo Currency ($RYO)—may play as an alternative in this dystopian future.

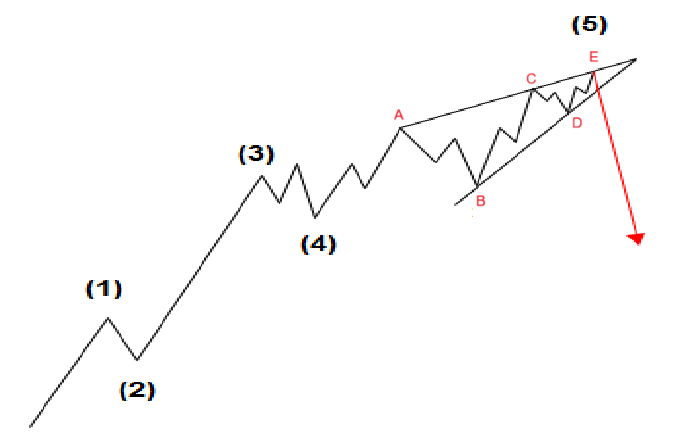

The Market’s Last Stand: An Ending Diagonal Pattern

Our technical analysis suggests that most global stock markets are in the final stages of an ending diagonal pattern, a formation that often signals the end of a major market trend. Currently, markets may be in the midst of completing a C wave or already navigating a corrective D wave, characterized by a downward trend. This phase is the precursor to the final E wave, which is expected to manifest as a dramatic blow-off top—a sharp, unsustainable surge in asset prices, usually even breaking out higher than the confines of the ending diagonal triangle.

This last rally will not stem from economic strength but from a desperate reaction to hyperinflation. As inflation spirals out of control, transitioning from high to full-blown hyperinflation, investors will pour into equities and other assets to preserve value, pushing markets to unsustainable heights. However, this surge will mark the tipping point, setting the stage for a devastating collapse.

Hyperinflation and the Bond Yield Trigger

Hyperinflation—where currency value plummets and prices soar—creates a self-reinforcing cycle of economic instability. In this environment, bond yields will spike as investors demand higher returns to offset the rapid erosion of purchasing power. Rising yields will increase borrowing costs for governments, corporations, and consumers, rendering debt unsustainable.

This spike in bond yields will act as the key trigger, igniting a massive sell-off in global stock markets. As equities plummet, the fallout will ripple through the financial system, unleashing contagion that destabilizes banks, investment funds, and other institutions. The result will be a severe liquidity crisis, where access to capital dries up, choking economic activity.

The Collapse of Traditional Finance

With liquidity evaporating, banks will likely impose a credit freeze, halting lending to safeguard their reserves. This will effectively shut down the monetary system, as businesses and individuals lose access to the funds they need to operate. ATMs and bank branches will close, leaving people stranded without cash or digital access to their savings. Confidence in fiat currencies will shatter, sparking social unrest and chaos as desperation mounts.

This breakdown will expose the fragility of the traditional financial system, pushing governments to intervene with radical measures to restore order.

CBDCs: A Surveillance-Driven “Solution”

Amid the turmoil, governments will introduce Central Bank Digital Currencies (CBDCs) as a supposed fix. Marketed as a stabilizing force, CBDCs will be rolled out rapidly, capitalizing on public desperation and the absence of alternatives. The transition will be seamless for most, as fear overrides resistance.

During this shift, existing fiat cash will linger as a stopgap, circulating alongside the new digital currency. However, its role will diminish as the old fiat is redenominated into the CBDC framework. Over time, paper currency will be phased out entirely, and all transactions will migrate to a digital infrastructure, granting governments unparalleled financial oversight and control.

CBDCs as a System of Surveillance

CBDCs are not merely digital versions of cash—they are tools of surveillance. Unlike traditional money, every CBDC transaction can be tracked, recorded, and analyzed in real time. This enables governments to monitor spending habits, enforce compliance, and even manipulate economic behavior through programmable money. Features like expiration dates, spending restrictions, or asset freezes could become standard, eroding personal financial autonomy.

The Digital Israeli Shekel: A Dystopian Example

The planned digital Israeli shekel exemplifies the dystopian potential of CBDCs. Israel’s central bank has been exploring this digital currency, which could include programmable features allowing the state to dictate how funds are used. For instance, the government might restrict purchases to “approved” goods, set expiration dates to force spending, or freeze accounts of dissenters—all without judicial oversight.

Israel’s development of the digital shekel, as highlighted in Cointelegraph’s report, heralds a transformative shift in its financial landscape—one that carries profound dystopian undertones. The push towards a cashless society, as noted in Bitcoin Magazine’s coverage, sets the stage for a financial system where every transaction is digital and, consequently, traceable. The elimination of physical currency amplifies the government’s ability to monitor citizens’ economic activities in real time. Every purchase, donation, or peer-to-peer transfer could be logged, creating a comprehensive profile of individual behavior. This level of oversight evokes a dystopian reality where financial privacy is extinguished, and the state wields unprecedented power over personal lives. The article suggests that this shift, while framed as a modernization effort, could enable authorities to freeze accounts or block transactions deemed undesirable—a tool ripe for suppressing dissent or enforcing compliance.

Reclaim the Net emphasizes the Bank of Israel’s efforts to boost the digital shekel’s adoption, spotlighting both its potential benefits and inherent risks. While the central bank touts efficiency and financial inclusion as key advantages, the article raises red flags about privacy concerns and government overreach. A CBDC like the digital shekel centralizes financial power, placing it squarely in the hands of the state. Unlike decentralized cryptocurrencies such as Bitcoin, which prioritize user autonomy, the digital shekel’s design would likely allow the Bank of Israel to dictate terms of use. This could include programming the currency with smart contracts—features that Cointelegraph notes are being explored in its accelerated development. Programmable money could impose expiration dates, restrict spending to “approved” categories, or penalize certain behaviors, transforming currency into a lever of social control. Imagine a scenario where funds allocated for welfare expire if not spent within a set period, or where purchases of politically sensitive materials are flagged or prohibited—such possibilities underscore the dystopian potential.

Further, Israel’s technical advancements in the digital shekel, including its reliance on blockchain technology, could enhance surveillance capabilities. Each transaction, immutably recorded on a digital ledger, becomes a permanent data point accessible to the state. Coupled with Israel’s existing technological prowess—demonstrated in the CoinGeek report on its successful blockchain-based bond tokenization pilot—this infrastructure could integrate financial data with broader surveillance systems. Israel’s history of leveraging technology for security purposes suggests that the digital shekel could seamlessly plug into a larger apparatus of control, merging economic and personal data into a single, all-seeing framework.

The risks extend beyond surveillance to systemic vulnerabilities. A fully digital currency is susceptible to cyberattacks, technical glitches, or deliberate manipulation by those in power. Centralization amplifies these threats: if the Bank of Israel’s systems are compromised, the entire economy could grind to a halt. Worse, the digital shekel could be weaponized to exclude specific groups—be it political adversaries or marginalized communities—creating a financial underclass unable to participate in the economy. This specter of exclusion, paired with the loss of cash as an anonymous fallback, paints a chilling picture of a society where financial autonomy is a relic of the past.

The Shift Towards a Cashless Society

Israel’s pursuit of the digital shekel is part of a broader global movement towards cashless societies, a trend that amplifies both the promise and peril of digital finance. This section examines this shift, contextualizing Israel’s efforts within worldwide developments and their implications for privacy, freedom, and inclusion.

Globally, nations like Sweden and China have pioneered the transition away from physical currency. In Sweden, cash usage has plummeted, with digital payments dominating everyday transactions; in China, mobile platforms like WeChat and Alipay have largely supplanted cash. Advocates argue that cashless systems enhance convenience, curb crimes like theft and money laundering, and streamline tax collection. Yet, these benefits come at a cost. The disappearance of cash eliminates the option for anonymous transactions, a cornerstone of financial privacy in free societies. Every digital payment feeds into a vast data ecosystem, ripe for exploitation by governments or corporations seeking to monitor or influence behavior.

In Israel, the government is actively accelerating this shift, as Bitcoin Magazine notes in its discussion of plans to go cashless. Legislative measures to restrict cash transactions, combined with the promotion of digital alternatives like the digital shekel, signal a deliberate move towards a fully digital financial system. The state frames this as a strategy to combat tax evasion and illicit activities, but the implications extend far beyond enforcement. A cashless Israel would render every financial interaction visible to authorities, stripping away the anonymity that cash provides. Small, everyday choices—buying a coffee, donating to a cause, or tipping a street vendor—would become data points in a permanent digital record, accessible to the state and potentially to private entities.

This transition poses significant risks. First, it threatens financial exclusion. Not all Israelis have equal access to the digital infrastructure required for a cashless economy—smartphones, reliable internet, or bank accounts may be out of reach for the elderly, low-income individuals, or rural residents. Without cash as a fallback, these groups risk being locked out of the financial system, deepening social inequalities. Second, the loss of cash erodes personal freedom. Anonymous transactions empower individuals to act without scrutiny; their absence subjects every financial decision to potential oversight, opening the door to behavioral manipulation through incentives or penalties.

Moreover, a cashless society concentrates power in the hands of central institutions like the Bank of Israel and the tech companies that support digital payment systems. This centralization introduces systemic risks: a cyberattack, power outage, or policy misstep could disrupt the entire economy. It also demands blind trust in these entities to prioritize public interest over control—a trust often undermined by historical precedent. The CoinGeek report on Israel’s blockchain bond pilot underscores the nation’s technical ambition, but it also hints at a future where financial innovation could tighten the state’s grip on economic life.

Cryptocurrencies: A Double-Edged Sword

As CBDCs dominate, cryptocurrencies could emerge as an alternative for those seeking to escape centralized control. However, their role is complicated by technological advancements in blockchain analytics and artificial intelligence (AI), which are advancing exponentially. These tools can de-anonymize transactions on public ledgers like Bitcoin ($BTC)’s, linking digital wallets to real-world identities. Even coins previously thought to be private, like Monero ($XMR), are increasingly being deanonymized with advancements in AI and machine learning, as discussed in this analysis on Ryo News, highlighting vulnerabilities in its privacy mechanisms.

Pseudonymous cryptocurrencies are becoming systems of surveillance, as governments and corporations harness AI to peel back layers of privacy. This erosion of anonymity undermines the original promise of cryptocurrencies as a bastion of financial freedom.

Privacy Coins: The Last Line of Defense

In this landscape, privacy coins stand apart, engineered to resist surveillance. While Monero has long been a leader in this space, its vulnerabilities to deanonymization have spurred the rise of alternatives that aim to deliver on the promise of true financial privacy. Among them, Ryo Currency emerges as a leading contender for true digital cash, offering robust privacy and decentralization in an increasingly monitored world.

Ryo Currency was developed with a focus on addressing the shortcomings of other privacy coins, prioritizing user anonymity and network decentralization from the ground up. Built on advanced cryptographic principles, Ryo aims to provide a secure and private financial ecosystem that withstands the growing threats posed by AI-driven surveillance and centralized control. Its commitment to privacy and user autonomy makes it a compelling option for those seeking to preserve financial freedom in a world where digital transactions are increasingly scrutinized.

Ryo Currency also fulfills a vision articulated by Nobel laureate economist Milton Friedman, who foresaw the rise of digital cash as a means to reduce government control. In 1999, Friedman predicted the development of a “reliable e-cash” that would enable anonymous transactions online, akin to handing over a $20 bill with no record of the exchange. He stated:

“So that I think that the internet is going to be one of the major forces for reducing the role of government. The one thing that is missing, but that will soon be developed, is a reliable e-cash. A method where buying on the internet, you can transfer funds from A to B, without A knowing B, or B knowing A. The way in which I can take a $20 bill and hand it over to you, and there is no record of where it came from.”

Ryo Currency embodies this vision by providing a digital equivalent of cash—transactions that are private, untraceable, and free from intermediaries—aligning perfectly with Friedman’s prophecy of a decentralized financial future.

Watch Milton Friedman’s prediction in his own words in this video:

Ryo Currency: Privacy and Decentralization Redefined

Ryo Currency leverages the Halo 2 Zero-Knowledge proofs protocol, the most advanced privacy technology available. Unlike other privacy coins that rely on ring signatures or mixers—methods vulnerable to sophisticated analysis—Halo 2 ZK proofs ensure that transactions are verified without revealing the sender, receiver, or amount. This mathematically provable privacy shields users from blockchain analytics, even as AI capabilities grow.

Additionally, Ryo Currency achieves true decentralization through its Cryptonight-GPU algorithm, which is resistant to Asic devices and botnets. This design allows mining with consumer-grade hardware, preventing the concentration of power in the hands of a few and preserving the network’s distributed integrity.

Conclusion: Navigating the Financial Future

The spike in bond yields will likely serve as the final domino, unleashing a cascade of hyperinflation, market collapses, and social disruptions. As traditional financial systems crumble, CBDCs will rise as a government-imposed solution, trading stability for surveillance. The digital Israeli shekel illustrates the dystopian risks of this shift, where programmable money could stifle individual freedom.

Cryptocurrencies offer hope, but their vulnerability to blockchain analytics and AI threatens their viability—except for privacy coins like Ryo Currency. With Halo 2 ZK proofs and the Cryptonight-GPU algorithm, Ryo stands as a beacon of privacy and decentralization, potentially the last refuge for those seeking true digital cash in a world of pervasive control.

As the global economy hurtles toward this tipping point, the choices we make—between centralized surveillance and decentralized freedom—will define the future of money and autonomy.